Mises Wire |

- Review: Chaining Down Leviathan: The American Dream of Self-Government, 1776–1865

- Ulrich Möller: The Video Game Industry Points to the Future of Organization Design

- Even the Fed Thinks Current Debt Levels Are Unsustainable

- Where Prices Come From: Menger Explains

- Don't Be Fooled by the Fed's Taper Talk

| Review: Chaining Down Leviathan: The American Dream of Self-Government, 1776–1865 Posted: 31 Aug 2021 12:00 PM PDT How is it that America became a "strong but limited" government, and the world's richest and most free country? That is the central question both considered and answered by Luigi Marco Bassani in his new work, Chaining Down Leviathan: The American Dream of Self-Government, 1776–1865. As an eminent scholar, Bassani has long studied the antebellum area, Amercia's struggle between national vs. local power, and the Jeffersonian tradition that colored the era. By combining all of these subjects into a single work, he endeavors to clarify the dynamics of political power in the early republic. As it turns out, the federal, decentralized framework that underscored the American political structure was its most distinct characteristic—a feature that is often ignored or downplayed by contemporaries. "The golden age of federalism and federal liberty," as Bassani puts it, resulted only from the multitude of self-governing societies that composed the federal union, all of which had a plausible claim to challenge the impositions of the federal government. Every command of the central authority, he writes, "was subject to be opposed and contained in a web of competing counterclaims." From the outset, Bassani promises to give the reader a very different interpretation of the antebellum period than they have likely been exposed to, and in this aim he succeeds. Rather than take all the claims of the Federalist advocates of the Constitution at face value, the author makes sure to give greater credit to those that opposed the framework. "The true defenders of the federal system were those who opposed the draft constitution, and they are fully entitled to be on equal footing in the history of American political thought," he declares. By this assertion, Bassani sets his work apart from virtually all others from the outset. In the tradition of Montesquieu, the Antifederalists were political realists that doubted a joint republic could long survive over such a vast territory as North America. By extension, they feared a strong executive, national court system, centralized law enforcement apparatus, and uniform system of taxation would soon grow to oppress the fledgling states. While they championed republican-oriented representation systems, they doubted that Congress would ever be truly representative enough—and even made attempts in several states, such as New York, to make the ratio of constituents to representatives greater than it was set to be in the House of Representatives. In all of this, Bassani proves that the Antifederalists were undeniably prophetic about the trajectory of national overreach in ways that practically leap off the pages. Most interestingly, he also demonstrates that Antifederalists were hardly the anarchist-driven zealots the Federalists often portrayed them as. Instead, they generally sought to amend the Articles of Confederation while still advocating constitutional government. Rather than reinvent the constitutional system, Bassani demonstrates that the group that opposed the Philadelphia Convention's proposal did so on the same basis that the American Revolution was waged—to preserve the local autonomy of each governing unit from transgressions from the central government. As he moves beyond the founding period, Bassani masterfully recounts the origins of the "Principles of '98," Thomas Jefferson and James Madison's strategy for combatting federal usurpation over reserved states' powers. According to both figures, each state—as the creators of the federal compact—could determine in the last resort whether that agreement had been violated. By extension, each state could nullify, or actively obstruct the enforcement of unconstitutional laws. As the two Virginians reasoned, granting the federal courts the same power unilaterally only guaranteed that the central government would gradually grow to oppress and subordinate the states into a dismal and unforeseen condition. To push their gambit forward, the two men crafted sets of resolutions for Virginia and Kentucky in 1798, both of which made a firm stand against the Alien and Sedition Acts of 1798. While the controversial acts were ultimately left to expire, and the Adams administration and Federalists in general were pushed out of power, clashes between the central government and the states continued in the ensuing decades. One of the most impressive parts of Bassani's narrative is its comprehensive treatment of forgotten events that followed in the footsteps of Jefferson and Madison's nullification doctrine. One example includes the federal attempt to conscript minors during the War of 1812, a plan that produced concerted hostility from New England. Prominent politicians from the region openly called for secession, others said the idea should be at least entertained. In the end, delegates from the northeastern states congregated in Connecticut for a meeting that became known as the Hartford Convention. While all states stopped short of declaring secession, several of them raised Jefferson and Madison's own prose to render the conscription law unauthoritative, void, and of no affect within their own states. If there is one aspect of the work that would shock laymen, I think this is it. In another invocation of nullification and self-determination, Bassani chronicles the Nullification Crisis of 1832 and its implications for federal versus state power. As the writer reveals, John Calhoun justified South Carolina's opposition to the federal tariff on the same foundations as Jefferson and Madison's political creed. Even as fire-eaters demanded secession in South Carolina, Calhoun stepped down from the vice presidency in opposition to Andrew Jackson, and defended the discharge of nullification as a happy medium that would keep his state in the union while still opposing what he deemed to be a bold-faced constitutional usurpation. Throughout the episode, Bassani explores the particulars of Calhoun's legal argument in ways that defy the manner in which the eminent South Carolinian is caricatured today. In the book's penultimate chapter, Bassani depicts Abraham Lincoln, the "herald of the modern state," as the true source a new, reinvented American political structure. Even before Lincoln's ascension to the presidency, the author reveals that Calhoun predicted in 1850 that the union was "doomed to dissolution" within the time frame of "twelve years or three presidential terms." Bassani demonstrates that from his first inaugural address onward, Lincoln—as the scion of Hamiltonian nationalism—subverted the federal framework in favor of a singular, homogenous nation-state. In stark contrast with the perception of the ratifying states as they adopted the Constitution, Illinois's favorite son portrayed the union as an inflexible, superlative, semisacred institution. As the author notes, this perception unambiguously denied the Jeffersonian construct of a utilitarian, decentralized league of states. Far from the "Great Emancipator," as he is sometimes called, Lincoln supported a constitutional amendment that would have barred the federal government from restricting or ending slavery for all time. Moreover, under his direction the federal government continued to enforce the despotic Fugitive Slave Act of 1850 long after the war had started, turned a blind eye to slavery in the states that remained loyal to the union, and reprimanded General John Fremont when he attempted to enact an exhaustive emancipation in conquered Missouri. Most significantly, Bassani artfully illustrates the manner in which the president disregarded the Constitution's original intent in the pursuit of his "perpetual union" creed. Indeed, Lincoln jailed hundreds of northern editorialists that criticized his administration, suspended the writ of habeas corpus, placed members of Maryland's legislature under house arrest such that they could not congregate, began a system of conscription for the first time in American history, instituted an income tax, and when Congress was not in session universally called forth an army of seventy-five thousand soldiers to invade the South. While Lincoln insisted the Southern states had no right to secede, he treated them nonetheless as independent enemy states for the purposes of waging war against them. By disregarding the originally ratified constitution, then, Lincoln ushered in a new era of political consolidation. With Chaining Down Leviathan, Bassani has assembled one of the most thorough and convincing defenses of federalism in the antebellum era, and in so doing, deconstructs prevailing American history narratives. Most importantly, the book reveals that decentralized government and states' rights were far from reactionary, postratification political strategies—they were the very cornerstones of the American political system. From every angle, the author reveals that it was the nationalist model of the union—rather than the federal counterpart—that was the counterrevolution to the federal compact between states. If it accomplishes nothing else, Bassani's formative account puts the final nail in the coffin of American nationalism. This posting includes an audio/video/photo media file: Download Now |

| Ulrich Möller: The Video Game Industry Points to the Future of Organization Design Posted: 31 Aug 2021 09:00 AM PDT Austrian economics has a lot to say about how to organize firms for maximum value generation. Austrian principles point to the delegation of entrepreneurial judgement to the front-line employees who interact directly with those who actually create value: users. The military organization models of the twentieth century, involving command-and-control in hierarchical structures, are slow to change, and the management literature evidences an unwillingness to abandon the hierarchy. But there is a fast-growing industry that's the locus of prodigious value generation where the hierarchy has already been abandoned and flat networks of distributed judgement are taking its place. Ulrich Möller is one of several Austrian economists who are studying the firms in the video game industry and demonstrating how their findings can bring positive organizational change to the rest of the business world (see our E4B Knowledge Graphic at Mises.org/E4B_133_PDF). Key Takeaways and Actionable InsightsOrganizational innovation has a long and successful track record in the video game industry.A lot of value has been generated in the video game industry in a short period of time. Video games surpass movies and music in revenue. Without a long history of corporate hierarchies and bureaucracy to shed, firms in the industry embraced the organizational innovations of open source software, including anonymous collaboration among highly distributed self-organized teams, peer review systems, and agile processes. In addition, the industry created its own laboratory for testing revolutionary organizational theories in virtual economies set in virtual worlds. Valve is a company in the video game industry that took organizational innovation to its logical conclusion: the end of hierarchy.Valve — a very successful, industry-leading company — pursued a value-generation logic to frame its approach to organization:

The answer? Let employees decide what to work on. Let them exercise entrepreneurial judgement. Let them, in effect, do both strategy and implementation. Give them all the decision rights. Let them identify customer preferences — since they know the customer best; let them decide how best to address those preferences; let them decide how to achieve competitive differentiation; let them allocate resources, choose costs, and manage profitability; let them control quality and decide when software is ready to ship. Employees work in self-organizing teams, and are free to migrate from team to team, and free to change their roles. There are no fixed job descriptions. In place of command-and-control, a few simple rules or constraints have emerged for the exercise of governance.F.A. Hayek wrote about norms that emerge in social groups to shape behavior. These are not legislation, i.e., written formal restrictions. They are what he called rules, constraints that everyone accepts in the shared commitment to collaboration and the pursuit of the most favorable outcomes. The most significant of these rules at Valve is the "Rule Of Three", a simple agreement that at least three individuals must agree on the initiation of a new project, or on other major decision points. The emergent standard was that this is just enough to prevent maverick behavior, and a low enough number to facilitate agile action that's not bureaucratically constrained. Another rule or constraint goes by the name of Social Proof. This is a broader and looser peer review standard. If the original team wishes to recruit more members, they must persuade others of the value generating potential of the project (in competition with other projects in the firm); successfully doing so constitutes "social proof" of value. Rules-based peer review process replaces management structure.Conventional approaches to organizational design focus on structure. This might be command-and-control hierarchy, or structured networks, or strategic business units or functional departments. Valve abandoned structural thinking and replaced it with flow analysis. How can we attract the most creative people to our venture? How can we encourage the most productive flows of bold creative thinking? How can teams best assemble and collaborate for the most productive output? How can we integrate with the user community in the best way? How can the most value-generative projects attract the best resources? These are all questions about flow. Austrian economists are distinctive in viewing capital as a flow rather than a structure, and this view holds true for human capital just as much as physical capital. Emergent rules for self-organizing human systems can perform all the managerial functions that were historically left to control structures. Actionable Insight Summary

Additional Resources"The Future of Organizational Design" — our E4B Knowledge Graphic (PDF): Mises.org/E4B_133_PDF "Levels without Bosses? Entrepreneurship and Valve's Organizational Design" by Ulrich Möller and Matthew McCaffrey: Mises.org/E4B_133_Paper1 "Entrepreneurship and Firm Strategy: Integrating Resources, Capabilities, and Judgment through an Austrian Framework" by Ulrich Möller and Matthew McCaffrey: Mises.org/E4B_133_Paper2 |

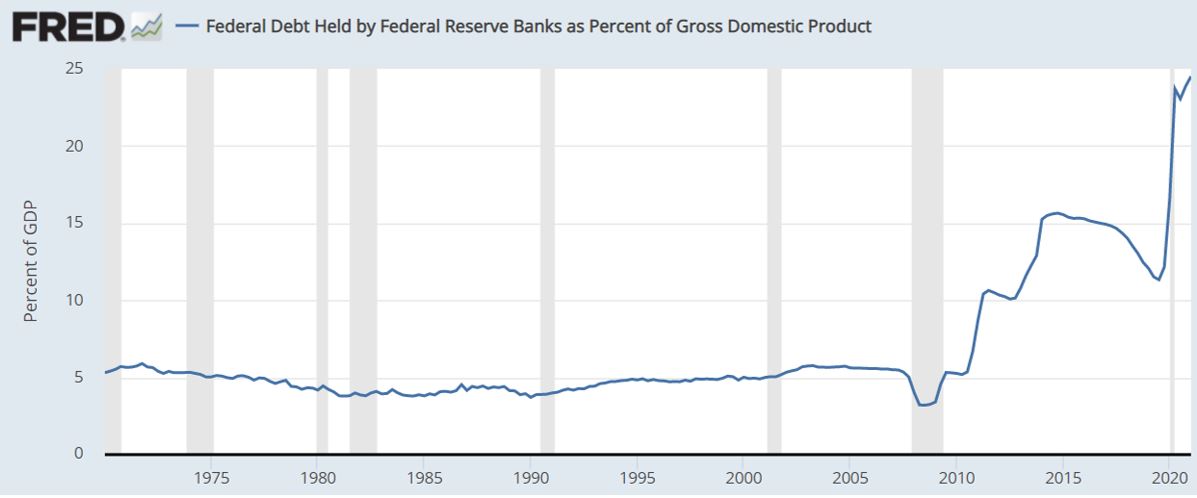

| Even the Fed Thinks Current Debt Levels Are Unsustainable Posted: 31 Aug 2021 09:00 AM PDT A few months ago US national debt exceeded $28 trillion. This number is certainly the one economists usually work with, but does this figure capture a long-term perspective? In March 2021, the Department of the Treasury published the 2020 Financial Report of the United States Government. In the initial message, Secretary Janet L. Yellen writes: "This Financial Report discusses not only current financial results but also important, long-term trends affecting our critical social insurance programs and fiscal health." The report not only discloses the current debt level, but also projects the cost of the government's future obligations to its citizens. It notes that citizens will have the right to demand benefits from the state in the future. The United States is one of the few countries whose treasury, in an act of transparency and with rigorous analysis, has warned its government of the unsustainability of the country's public finances. The US Department of the Treasury anticipates that unless there are substantial changes, the system will not be sustainable: "If changes in policy are not so abrupt as to slow economic growth, then the sooner policy changes are adopted, the smaller the changes to revenue and/or spending [that] will be required to return the government to a sustainable fiscal path." Government reports on macroeconomic matters tend to be ambivalent. Nevertheless, this one's conclusion is decisive: the US government's fiscal policy is unsustainable. The Primary DeficitThe report usefully distinguishes between the primary deficit and the total deficit. Generally speaking, the primary deficit does not include the cost of servicing the debt (i.e., interest) while the total deficit does. To conduct a rigorous analysis of public finance sustainability, it is appropriate to consider the primary deficit, because if there is a structural primary deficit, it is difficult for a country to achieve long-term sustainability no matter the interest rate. The Fed could help the government lower the total deficit with a rate decrease, but major structural changes are needed to lower the primary deficit. The following graph, which appears in the report, compares total fiscal receipts, represented by the black line, with total structural expenditure. When the line representing total receipts (the thick black line) is below the sum of the various budget expenditure items, there is a primary deficit. During the years of the financial crisis (2009–12), the deficit-to-GDP ratio spiked, and it skyrocketed again in 2020 due to increased spending to address covid-19. Chart 1: Comparison of Each Major Category's Weight with Respect to Tax Revenues  Source: US Department of the Treasury, Financial Report of the United States Government, FY 2020, Mar. 25, 2021.The Department of the Treasury assumes there will be a structural primary deficit and that total deficit (represented by the difference between the blue line and the thick black line), which includes the cost of servicing the debt, will increase with time. The report continues with a graph that illustrates how, if the trend continues, the government's debt could reach 300 percent of GDP in less than forty years.  It is important to clarify that the above graph only considers "debt held by the public," currently around 100 percent of GDP; however, if debt held by Federal Reserve Banks were included, the total debt would be 130 percent of GDP. The Fed argues that this additional $6 trillion debt should not be considered because "Federal Reserve Banks remit their profits to the Treasury, [and] any interest earned on their federal debt is rebated to the federal government." But if the Fed continues to increase its position relative to US debt, this consideration might need to be reviewed.  In any case, the Department of the Treasury projects the future debt of the government and calculates that it could triple GDP within forty years. If the Federal Reserve Banks' debt were consolidated, this threshold would be reached in much less time. A country with a welfare state commits to offering its citizens future benefits (principally pensions and health services) using taxes collected in the present. While tax revenues are accounted for upon collection, government's future obligations are not. What would happen if we accounted for the obligations in present value terms? This is exactly what the Department of the Treasury does in its analysis. US companies that agree to provide their employees with future pensions (which the companies have to finance) have to budget annually to satisfy their future payment obligations in accordance with US Generally Accepted Accounting Principles (GAAP). But the government is not required to make provisions to cover future benefits, currently doing so only for federal employees and veterans. What Would the Debt Figure Be If the United States Calculated the Present Value of Future Obligations?The Department of the Treasury declares that "[t]he long-term fiscal projections indicate that the government's debt-to-GDP ratio will rise to 623 percent over the 75-year projection period, and will continue to rise thereafter, if current policy is kept in place." Just to give an idea of how fast the debt-to-GDP forecasts are increasing, the same report two years ago estimated that same ratio would rise to 530 percent in that period. Let's see why the debt is projected to become more than six times GDP. First, considering a seventy-five-year projection period, the net present value of future tax revenues is estimated to be $295.4 trillion. From this the present value of future noninterest spending—$374.9 trillion—must be subtracted. The main projected expenditures are on social insurance—that is, healthcare and pensions.  The Statements of Long-Term Fiscal Projections (SLTFP) shows that the present value of total noninterest spending, including Social Security, Medicare, Medicaid, defense, education, etc., over the next seventy-five years under current policy is projected to exceed the present value of total receipts by $79.5 trillion. Social insurance net expenditures (Social Security and Medicare) account for $65.5 trillion of this noninterest spending. However, these projections fix variables that the calculation of payment obligations is very sensitive to, such as the fertility rate, life expectancy, and average annual growth in health costs. Much like in the majority of developed countries, the fertility rate (defined as number of children per woman) in the United States showed a downward trend. In 2007 this ratio was 2.1 percent while in 2020 it reached 1.64 percent, a record low. Is it realistic to assume that fertility rate will return to 2.0 and remain stable for the next seventy-five years, as the Treasury's projections assume? Using an assumed fertility rate of 1.8 percent (closer to the current one) instead of 2.0 percent increases the financing shortfall by $2.5 trillion. The same is true for average annual growth in health costs: if 4.7 percent is used instead of 3.7 percent, $14 trillion more in debt are added. The Department of the Treasury also assumes the country will not disintegrate. Therefore, it calculates the present value of future revenues and obligations into the indefinite future (valuations by companies similarly assume they will operate indefinitely):

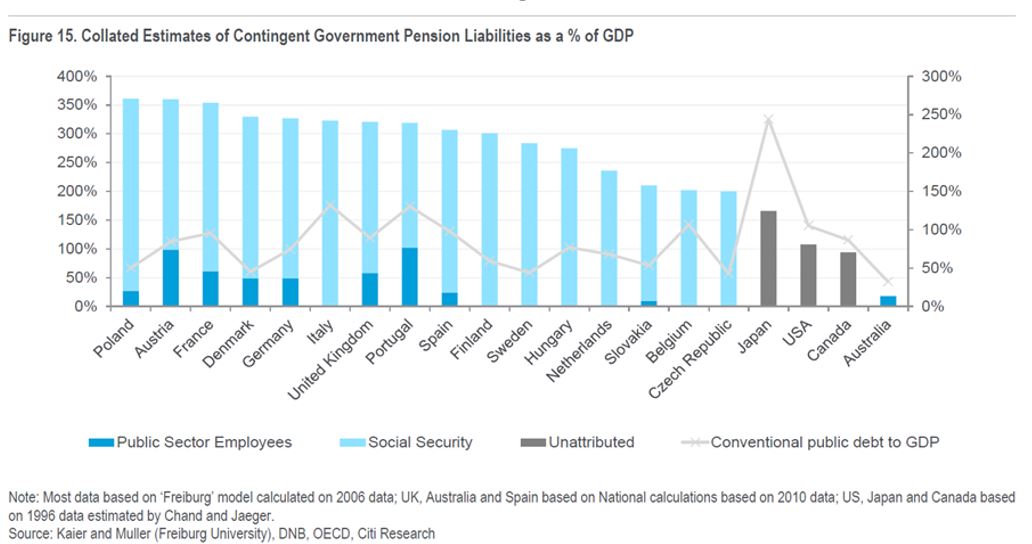

With these adjustments, the present value of future costs less the present value of future income rises to $154 trillion, and let's recall that this figure does not include interest expenses nor the debt held by the Fed in their books. What Is the Situation in Other Countries?Unfortunately, the same analysis applies to other countries. In fact, some years ago Citigroup calculated what the debt would be if future government pension liabilities were accounted for in present value terms. Note that the report only includes expenditures on pensions.  As can be seen in the graph, the majority contingent government pension liabilities in most European countries reached a present value of three times their GDP. ConclusionEconomists need to warn the public of the unsustainable nature of our governments' public finances. Only then will our political leaders be able to debate measures that might reverse the undesirable trends. Not much can be added to what has been exposed in the US government's financial report, and its conclusions speak for themselves:

This posting includes an audio/video/photo media file: Download Now |

| Where Prices Come From: Menger Explains Posted: 31 Aug 2021 08:00 AM PDT Because people strive to improve their condition, they exchange goods and, in this sense, they create the necessary conditions for the emergence of prices. Prices are simply an unintended consequence of the human quest to improve one's life. Original Article: "Where Prices Come From: Menger Explains" This Audio Mises Wire is generously sponsored by Christopher Condon. Narrated by Michael Stack. |

| Don't Be Fooled by the Fed's Taper Talk Posted: 31 Aug 2021 06:00 AM PDT There won't be a taper tantrum if the Fed seriously moves toward tapering. Investors now understand how the game works. Tapering doesn't actually mean the end of monetary inflation, and everyone knows it. Original Article: "Don't Be Fooled by the Fed's Taper Talk" This Audio Mises Wire is generously sponsored by Christopher Condon. Narrated by Michael Stack. |

| You are subscribed to email updates from Mises Wire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

{kind=link}

{kind=link}

No comments:

Post a Comment